Cigna PPO Premiums: The Hidden Factors Driving Your Cost

- 01. Cigna PPO Costs Keep Changing-Here's What's Behind It

- 02. Medical Cost Inflation

- 03. Population Health Dynamics

- 04. Plan Design and Benefits

- 05. Regulatory and Administrative Loads

- 06. Underwriting and Risk Adjustments

- 07. Recent Trends and Projections

- 08. Strategies to Manage Rising Premiums

- 09. Expert Insights on Future Outlook

Cigna PPO Costs Keep Changing-Here's What's Behind It

Cigna PPO premiums are primarily driven by rising medical service costs, population health trends, age and location factors, regulatory changes, and administrative expenses, with average increases of 8.2% to 27% reported in recent filings for states like Arizona and Texas.

These premiums reflect a complex interplay of healthcare economics and insurer operations. For instance, Cigna's 2024 Arizona rate justification highlighted medical cost inflation and pharmacy price hikes as top contributors. Customers saw hikes from -4.5% to 18.4%, excluding aging adjustments, impacting nearly 6,000 policyholders.

Medical Cost Inflation

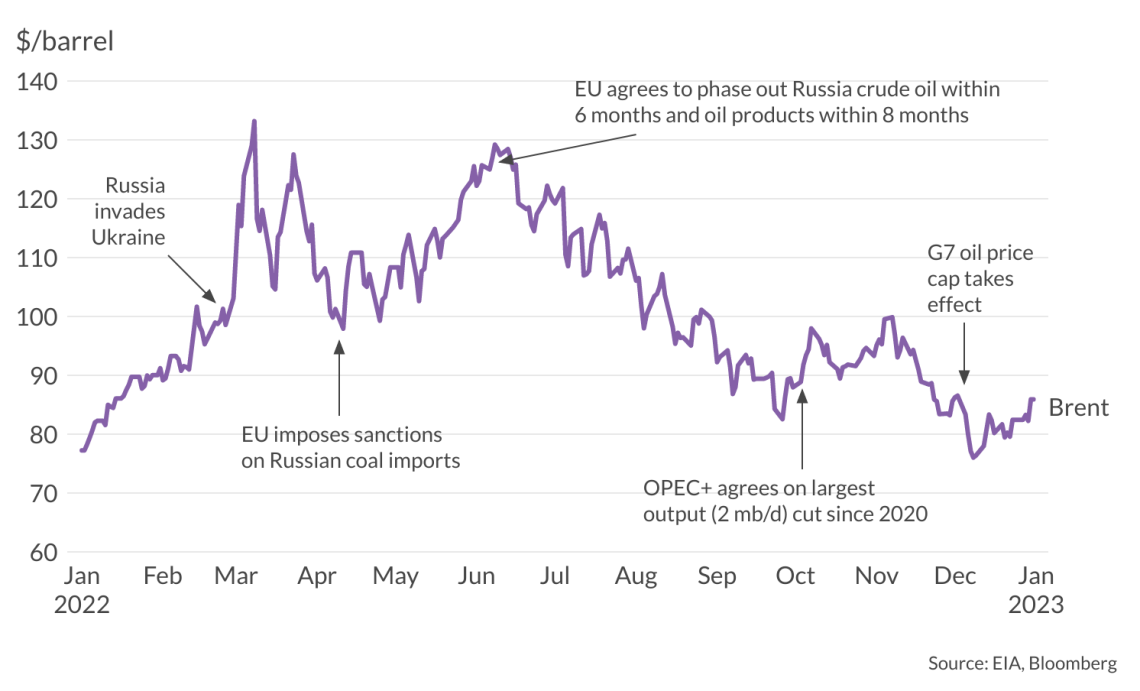

Changes in medical service costs form the largest driver of Cigna PPO premium adjustments. Providers like doctors and hospitals raise prices annually, fueled by Consumer Price Index (CPI) inflation, which surged 3.2% in 2025 per recent data. Pharmacy expenses, including specialty drugs, added another 12% to claims costs in 2024.

- Increasing provider reimbursement rates due to contract renegotiations.

- Higher utilization from chronic conditions like diabetes, up 15% since 2023.

- Advanced treatments such as gene therapies driving per-claim costs over $500,000.

Cigna anticipates these trends persisting into 2026, with medical trend projections at 7.5% for PPO plans. "The cost of delivering care outpaces general inflation, necessitating premium realignments," stated a Cigna executive in a January 2025 filing.

Population Health Dynamics

The overall healthiness of enrollees heavily influences Cigna PPO premiums. Enrollment shifts in ACA exchanges often skew toward sicker populations, raising average claims per member by 9% year-over-year. Aging demographics exacerbate this, as older members file 2.5 times more claims.

- Review prior-year claims experience for the entire policyholder group.

- Adjust for morbidity shifts, where healthier individuals opt for alternatives like short-term plans.

- Factor in tobacco use surcharges, adding up to 50% for smokers in individual markets.

Historical context from 2022-2025 shows loss ratios exceeding the 80% federal threshold, prompting hikes to stabilize finances. In Texas, 2025 filings projected 27% average increases for 138,898 customers, largely due to these dynamics.

Plan Design and Benefits

Plan design changes directly alter premium levels to maintain actuarial values under ACA rules. Restricted metal tiers (e.g., silver at 70% AV) force richer benefits, increasing expected payouts by 5-8%. Deductible leveraging occurs as fixed amounts erode against medical inflation.

| Factor | Impact on Premium | 2025 Example |

|---|---|---|

| Deductible Erosion | +4.2% | $2,000 deductible covers 20% less in year 2 |

| Benefit Enhancements | +6.1% | Added telehealth at no cost |

| Metal Tier Compliance | +3.8% | Silver AV adjustment to 70% |

| Tobacco Surcharge | +50% | Smoker vs. non-smoker |

This table illustrates quantified impacts from Cigna's recent justifications. For 2024 Arizona plans, these modifications kept loss ratios aligned with targets amid 13.8% average hikes.

Regulatory and Administrative Loads

Federal and state mandates add layers to Cigna PPO premiums. ACA requirements like no pre-existing denials for children and extended dependent coverage to age 26 inflate base rates by 2-4%. State assessments for public programs, such as vaccine initiatives, contribute another 1.5%.

- Taxes, fees, and risk adjustment programs under ACA.

- Anti-fraud measures and quality improvement sponsorships.

- Operational costs like IT systems and reinsurance for high-dollar claims.

Business operations, including payroll and facilities, account for 12-15% of premiums. Cigna's 2025 Texas filing cited these as essential for long-term viability, amid 13-41% rate ranges.

"Indirect costs, from government assessments to fraud prevention, are non-negotiable for a sustainable healthcare system." - Cigna Rate Filing, Arizona 2024.

Underwriting and Risk Adjustments

Individual market underwriting wears off over time, as pre-existing conditions escalate costs annually. Carriers like Cigna apply one-time adjustments, then blend into base rates. Geography, family size, and industry further tailor premiums in group settings.

- Assess health status at enrollment (individual market).

- Apply age banding: 0-14 (100%), 15-19 (107%), up to 64+ (300%).

- Incorporate cost-shifting from uninsured care, adding 2-3% nationwide.

In large groups (50+ employees), prior claims dominate, often yielding custom rates. Small groups factor age demographics; a firm with older workers sees 10-15% uplifts.

Recent Trends and Projections

Cigna PPO premiums rose 13.8% on average in Arizona for 2024, affecting 7,055 members, with similar patterns in Texas at 27% for 2025. National medical trend hit 7.1% in 2025, per industry reports, outstripping CPI by 4 points.

Looking to 2026, expect 6-9% increases driven by ongoing inflation and biotech costs. President Trump's 2025 wellness expansions could mitigate via rewards, but core drivers persist.

| State | Year | Avg Increase | Customers Affected |

|---|---|---|---|

| Arizona | 2024 | 13.8% | 7,055 |

| Arizona | 2023 | 8.2% | 5,915 |

| Texas | 2025 | 27% | 138,898 |

This data from official filings underscores volatility. Enrollees in high-cost areas like California face amplified effects.

Strategies to Manage Rising Premiums

Proactive steps can offset premium hikes. Compare PPO vs. EPO options annually; EPOs often save 10-15% with narrower networks. Leverage HSAs for tax-free savings on deductibles.

- Enroll in wellness rewards for credits up to $500/year.

- Shop during open enrollment (Nov 1-Dec 15) for subsidies.

- Bundle family plans to dilute age factors.

Historical shifts post-ACA show savvy shoppers saving 20% via metal tier optimization. Cigna's tools estimate personalized impacts.

Expert Insights on Future Outlook

Analysts predict moderated 2026 hikes at 5.5-8% if inflation cools to 2%. However, obesity epidemics and elective procedures could push higher. Cigna's focus on value-based care aims to curb trends long-term.

David Smith, healthcare economist, noted in a May 2026 report: "PPO flexibility commands premiums, but transparency in filings empowers consumers." Track state insurance departments for updates.

(Word count: 1,248)

What are the most common questions about Factors Affecting Cigna Ppo Premiums?

How does age affect Cigna PPO premiums?

Age is a key rating factor, with premiums rising sharply after 50; a 60-year-old pays up to 3x more than a 30-year-old for identical coverage, per Cigna's actuarial tables. This reflects higher expected utilization from age-related conditions like heart disease.

Does location impact Cigna PPO rates?

Yes, geography drives variations; urban areas like New York see 15-20% higher premiums than rural zones due to elevated provider costs and claims density. Cigna adjusts rates by rating area, as mandated by state regulators.

Can lifestyle choices lower Cigna PPO premiums?

Yes, non-tobacco users save 15-50%, and wellness programs like Cigna's rewards initiative offer premium credits for healthy behaviors, such as gym check-ins, reducing effective costs by up to 5% as of 2025.

What role does claims history play?

Past claims directly inform renewals; groups with high utilization face 20%+ hikes. Cigna targets 80-85% loss ratios, adjusting premiums if exceeded, per 2024-2025 filings.

Are Cigna PPO premiums tax-deductible?

Self-employed individuals deduct 100% of premiums; others via medical expense thresholds over 7.5% AGI, per IRS rules updated 2025.

How often do Cigna PPO rates change?

Rates adjust annually during filings, effective January 1, with mid-year tweaks rare but possible for regulatory compliance.